When War Breaks Out

The Moment Markets Fear War the Most

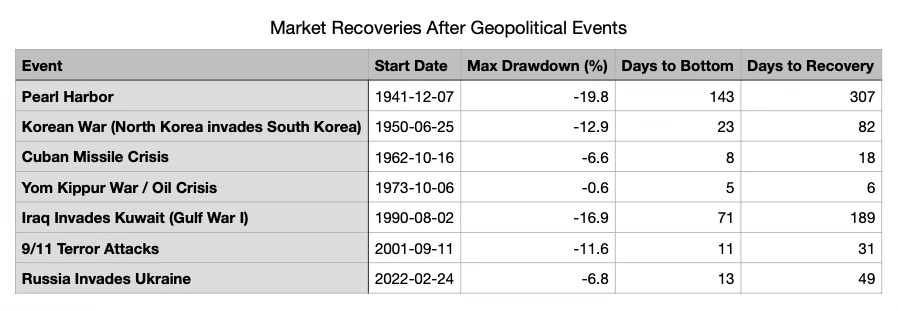

Armed conflicts are a wretched fact of life. When war breaks out, it is natural for investors to assume the market will collapse. Yet, history suggests something stranger, that markets often do not fall very far. And when stocks sink, they rarely stay down for long, as shown in the sampling below.

The fact that markets tend not to fall far is a destabilizing one. Why? Because if markets routinely recover within weeks of geopolitical shocks, then the most common investor reaction is to reduce exposure once the conflict begins.

That reaction is often a bigger problem because it addresses the wrong moment.

The Event Everyone Watches

The outbreak of war feels like the decisive point. Each arrives with a sense that the world has just crossed a threshold. News anchors speak of escalation. Strategists warn of uncertainty. Investors feel the pressure to reposition.

The logic seems obvious: if war is bad for markets, the moment it begins should be the most dangerous moment to hold equities.

But market history does not behave that way.

What Actually Happens

Across many geopolitical shocks, a pattern appears. Markets do decline, both those declines tend to be modest.

More importantly, they tend to reverse far faster than most investors expect. Many recover within a few weeks. This is not because war is economically harmless. It is because markets rarely collapse over events that are already visible.

Once the event occurs, a crucial variable—uncertainty—disappears.

As discussed in this publication previously, markets discount widely known information.

The Market’s Real Enemy

Markets struggle most when outcomes cannot be bounded. Before a conflict begins, investors imagine multiple catastrophic scenarios:

Energy systems collapse.

Supply chains fracture.

Superpowers enter direct confrontation.

Those possibilities create fear. But once the conflict actually starts, something subtle changes. The range of plausible outcomes narrows. Even if the situation remains dangerous, investors now have information.

And markets price information far more easily.

The Misidentified Risk

If this pattern is well documented, why do investors continue to respond the same way?

Because the psychological sequence runs opposite to the market sequence. Investors feel the most fear after the event becomes visible. Markets often feel the most fear before.

This mismatch creates a familiar outcome: Investors reduce risk precisely when markets are beginning to stabilize.

Most investors believe the danger lies in being invested when the crisis begins. But historically, the greater danger has been something quieter. Reacting to the crisis after it begins. Selling after the initial shock. Waiting for “clarity.”

Clarity rarely arrives before prices move.

The Question That Matters

None of this means geopolitical events are irrelevant. Some do produce prolonged market damage. The worst pullbacks (pre-2000) often occurred when war coincided with a recession or energy crisis (e.g., 1941, 1990).

But those cases share a different feature. They coincide with deeper economic disruptions—energy shocks, recessions, structural financial stress.

War alone is rarely enough. The market is not reacting to the event itself. It is reacting to whether the event changes the economic system.

So when the next geopolitical crisis erupts, the most useful question is:

“In what way does this event fundamentally alter the structure of the global economy?”

If the answer is “it doesn’t”, the historical pattern is remarkably consistent. The shock of conflict fades faster than the fear.

Avoid Self-Sabotage

The common belief is that wars trigger prolonged market collapses. The historical record suggests something else. Markets struggle most with uncertainty, not with events.

And the outbreak of a conflict often resolves more uncertainty than it creates. The practical implication is uncomfortable. The moment that feels most dangerous to investors has often been the moment when the market’s worst fears were already behind it.

Not always. But often enough that reacting instinctively to geopolitical headlines has become one of the most reliable ways investors sabotage their own long-term outcomes.

This publication is for brains, not bets. The Other Side of Obvious shares ideas, stories, and general financial information - not personalized investment, tax, or legal advice. Investing comes with risk (including losing money). Talk to a pro before you act. Please take time to read these important disclosures before you get started.

Interesting thoughts!Thank you for sharing!