The Leading Economic Index

One of the best (and overlooked) tools for investors

There is a peculiar habit in markets to fixate on the present. Yet, the most valuable signals are those that point forward. After all that’s what stock prices do. They point forwards ~ 12-18 months.

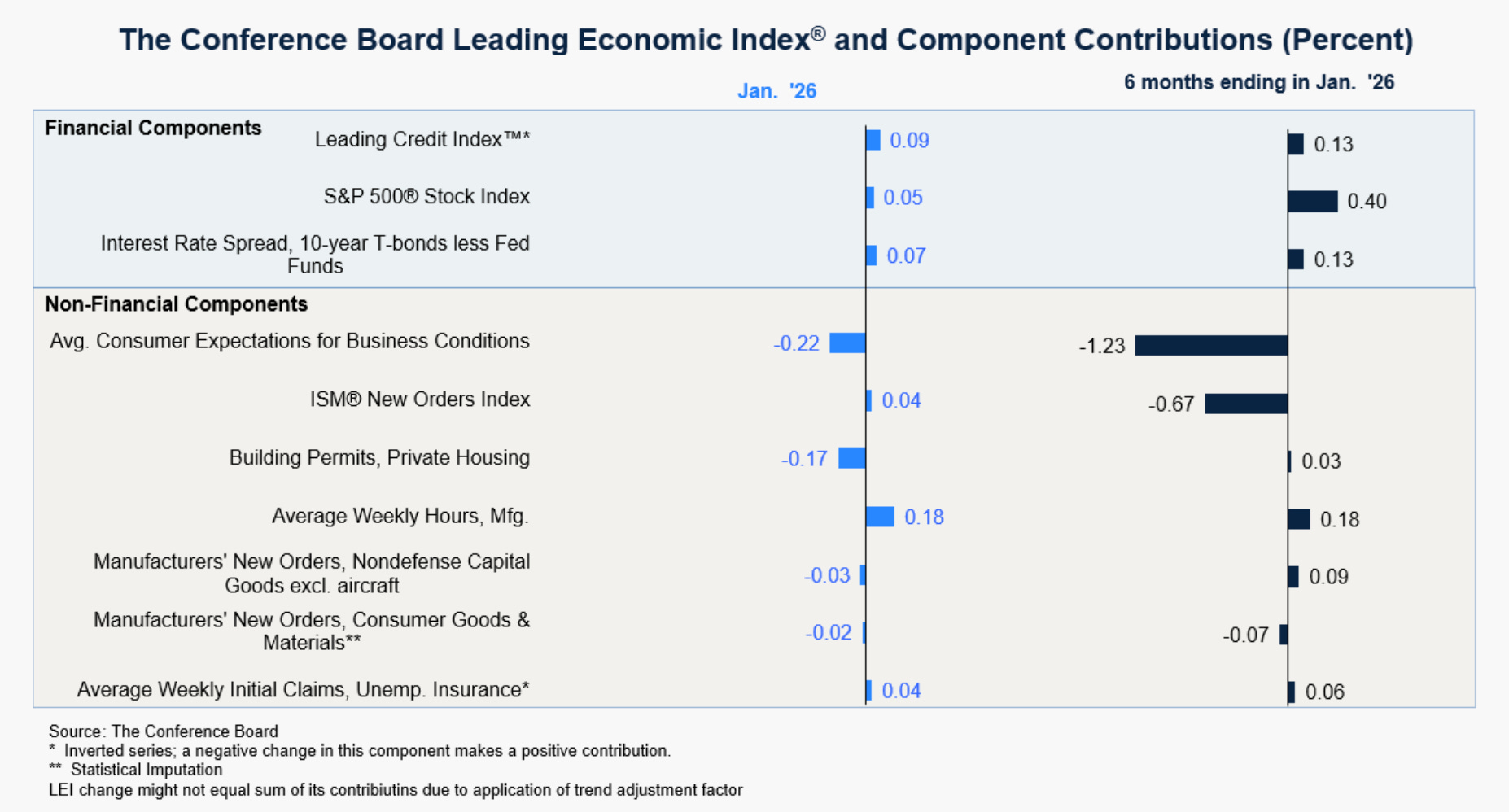

Among those forward looking signals is the Leading Economic Index (LEI), published by The Conference Board. The LEI is a composite of ten forward-looking components that, taken together, provide a reliable sketch of the economic future.

One would think that at present the LEI would be flashing red. Instead it is gradually drifting downward. And that is precisely what makes it so difficult to interpret and so dangerous to ignore.

The Shape of the Present

The LEI today resembles a slow seepage. Month after month, small declines have accumulated.

If one were to plot it against history, the current profile would not resemble the dramatic plunges preceding the 2008 Financial Crisis or the sudden shock of the COVID-19 pandemic. It is among the more ambiguous episodes such as 1995, 2015, perhaps the early stages of 2006.

The economy, in other words, is not falling off a cliff. The present moment most closely resembles a pre-decision phase. The economy is still expanding and the labor market is holding. Yet underneath, forward momentum has thinned.

The Soft Landing Question

A “soft landing” occurs essentially when inflation subsides, growth slows but does not contract, unemployment rises only modestly, and financial markets continue their upward drift.

The LEI, historically, has occupied a paradoxical role in such moments. It often turns negative before the economy weakens meaningfully and long before markets react.

Consider three cases:

1. 1995–1996: The Classic Deceleration

The LEI flattened and dipped. Growth slowed. The Federal Reserve eased. No recession followed.

Outcome: Equities surged; the expansion resumed with vigor.

2. 2015–2016: The Industrial Scare

The LEI declined modestly, dragged by global weakness and manufacturing softness.

Outcome: A correction occurred, then recovery. No systemic break.

3. 2006–2007: The Deceptive Plateau

The LEI rolled over gradually. Nothing appeared urgent. Markets continued rising.

Outcome: A delayed but catastrophic repricing.

The same signal produced radically different futures.

Why the LEI Is So Often Overlooked

If the LEI is so useful, why is it so frequently ignored? You don’t really hear much about it from mainstream media.

First, the LEI lacks the immediacy of the snake-oil charm we read from a growing portion of financial and economic reporting. In other words, it lacks drama. It fails to command attention simply because its message is incremental. Slow and incremental usually equals boring.

But the LEI also conflicts with present data, such as employment data, earnings reports, etc. To listen to the LEI can feel like betting against the present reality. And that’s actually the beauty of it.

The probabilistic nature of the LEI means it doesn’t make declarations. It provides the odds by which investors and portfolio managers can perceive the future. For traders, it isn’t much help.

The LEI as a Portfolio Tool

For the investor willing to listen, the LEI provides a way of understanding the economic landscape in which returns are generated.

When the LEI is rising it signals that growth is broadening; a condition in which risk assets tend to perform well. When the LEI is falling (as now), forward returns become more dispersed.

Practical implication? The LEI is not necessarily signaling an exit from equities. But it suggests a moderation of exposure in favor of quality stocks and reduced leverage.

In late-cycle LEI regimes, leadership often shifts from cyclicals to defensives and from speculative growth to cash-generative firms (i.e., those with endurance).

The LEI rarely acts alone. Its warnings become more actionable when confirmed by rising unemployment, credit spreads widening and/or yield curve re-steepening after inversion.

Timing Expectations, Not Markets

Perhaps the most subtle use of the LEI is its ability to recalibrate expectations. This is highly significant for mitigating the psychological effects of investing.

In declining LEI environments, strong market returns are less reliable. There tends to be an increase in volatility. And, the narrative shifts increase in frequency. All of which requires measured posture by self-investors.

The LEI does not predict catastrophe. It suggests that the economy has entered a regime where outcomes are no longer tightly clustered. Where the range of plausible futures has widened.

A soft landing remains entirely possible. History offers several such precedents. But those same histories remind us that the path from slowdown to stability is narrow and easily disrupted.

This publication is for brains, not bets. The Other Side of Obvious shares ideas, stories, and general financial information—not personalized investment, tax, or legal advice. Investing comes with risk (including losing money). Talk to a pro before you act. Please take time to read these important disclosures before you get started.

very educational, thks of sharing